Home » What is Part D?

What is Part D?

Medicare Part D is a federal program administered through private insurance companies. These companies offer retail prescription drug coverage to Medicare beneficiaries. Prior to 2006, when Medicare Part D began, many Medicare beneficiaries in America had little help with retail drug costs. They would often spend thousands of dollars each year paying for their medications out of pocket.

Fortunately, today’s Medicare beneficiaries have better coverage with Part D. Beneficiaries can enroll in a standalone Part D drug plan that goes alongside their Original Medicare benefits, or they can choose a Part D drug plan that is built into a Part C Medicare Advantage plan. Either way, Part D offers seniors some much-needed help with prescription drug costs.

What is Part D and how does it work?

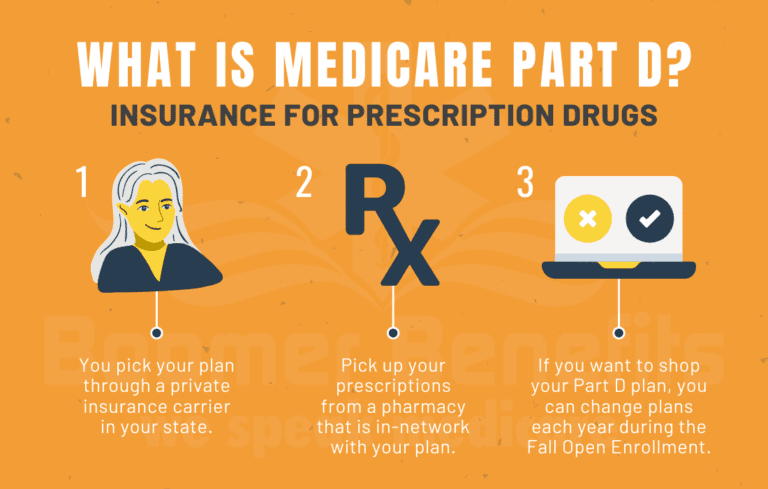

What is Part D?

Part D is an optional prescription drug program for people on Medicare. You pay a monthly premium to an insurance carrier for your Part D plan. In return, you use the insurance carrier’s network of pharmacies to purchase your prescription medications. Instead of paying full price, you will pay a copay or percentage of the drug’s cost. The insurance company will pay the rest.

Your Part D insurance card will be separate from your Medigap plan.

Medicare Part D plans all follow federal guidelines. Each insurance carrier must submit its plan outline to the Centers for Medicare and Medicaid Services annually for approval.

To improve your understanding of Medicare Part D, let’s look at the basic way that each Part D plan works:

How Does Medicare Part D Work for Seniors?

There are four stages to a Part D drug plan: the annual deductible, initial coverage, the coverage gap, and catastrophic coverage.

- Annual Deductible: In 2022, the allowable Medicare Part D deductible is $480. Plans may charge the full Part D deductible, a partial deductible, or waive the deductible entirely. You will pay the network discounted price for your medications until your plan tallies that you have satisfied the deductible. After that, you enter initial coverage.

- Initial Coverage: During this stage of Part D drug coverage, you will pay a copay for your medications based on the drug formulary. Each drug plan will separate its medications into tiers. Each tier has a copay amount that you will pay. For example, a plan might assign a $7 copay for a Tier 1 generic medication. Maybe Tier 3 is a preferred brand name for a $40 copay, and so on. The insurance company tracks the spending by both you and the insurance company until you have together spent a total of $4,430 in 2022.

- The Coverage Gap: After you’ve reached the initial coverage limit for the year, you enter the coverage gap. During the gap, you will pay only 25% of the retail cost of your medications. (This is so much better than in 2006 when many people had to pay 100% of their drugs in the gap.) Your gap spending will continue until your total out-of-pocket drug costs have reached $7,050 in 2022. Please note that to get into the gap, Medicare tracks the total costs of what you and the insurance company have spent, but to get OUT of the gap, they are counting only what you have paid in deductibles, copays, and gap spending that year, plus manufacturer discounts. They do not count anything the federal government contributes.

- Catastrophic Coverage: After you’ve reached the end of the coverage gap, your plan will kick in to pay 95% of the costs of your formulary medications for the rest of the year. This feature in Part D drug plans helps you limit your potential spending if you have expensive medications.

Medicare Part D Explained

Medicare Tracks Your Part D Spending

It’s important to note that Medicare tracks your True Out of Pocket Costs (TrOOP) for each year. This can protect you from paying certain costs twice. For example, if you have already satisfied the deductible on one plan and then later switch to a different Medicare Part D plan mid-year because you move out of state, your new plan will already see that you have paid the deductible for that year. The costs for the coverage gap and catastrophic coverage work the same way.

Part D drug plans also change from year to year. Your plan’s benefits, formulary, pharmacy network, provider network, premium, and/or co-payments/co-insurance may change on January 1st. Medicare gives you an Annual Election Period during which you can change your plan if you desire to do so.

Drug utilization rules that affect your Part D coverage

As a Medicare recipient, you may be subject to certain drug utilization rules that could affect your Part D coverage. These rules are in place for safety reasons and/or to help contain costs. The most common utilization rules that you may come across are:

Quantity Limits – There may be a restriction on how much medication you can purchase at one time or with each refill. If your doctor prescribes an amount that exceeds the quantity limit, the insurance company will likely require him or her to submit an exception form explaining the need for the additional medication.

Prior Authorization – You or your doctor may be required to obtain approval from the plan before a pharmacy can dispense your medication. The insurance company may request proof that the prescription is medically necessary before they agree to cover it. This is typically done for medications that are expensive or very potent. The doctor must be able to show why this specific medication is necessary for you and why alternative drugs might be harmful or ineffective.

Step Therapy – The plan may require you to try less expensive alternative medications that treat the same condition before they will consider covering the prescribed medication. If the alternative medication is effective, both you and the insurance company can save money. If it is not effective, your doctor will need to assist you in filing a drug exception with your carrier to request coverage for the original medication prescribed. He or she will need to explain why you need the more expensive medication when less expensive alternatives are available. Often this requires that he or she shows that you have already tried less costly options that were not effective.

Your overall Medicare prescription costs can be affected by these restrictions. Always check your medications in the plan formulary to see if restrictions apply to any of your important medications.

Restrictions are Part of All Part D Drug Plans

It’s important to understand that all Part D drug plans have some sort of restriction in place – especially for pain medications, narcotics, and opiates. This means that no matter which plans you choose, you’ll likely have to deal with extra paperwork on a regular basis.

The best way to approach this is by first finding the Part D drug plan with the lowest overall annual spending. Then, you can file the required exception forms in order to try and get as much approval as the plan will allow.

There are also some medications that aren’t covered by Part D at all. If you take one of these medications – such as a compound medication – you’ll have to file an exception in order to try and get the drug approved. However, not all exceptions are approved. So it’s important to be aware that you may end up paying for some medications out of pocket.

Overall, Part D drug plans can be quite confusing – especially for senior citizens. That’s why it’s so important to make sure that you understand your plan’s formulary and what medications are covered. You don’t want to be caught off-guard and have to pay for something that you thought was covered.

Frequently Asked Questions:

Do I have to pay for Medicare Part D?

No, you will not have to pay for Medicare Part D if you qualify for Medicare’s Extra Help Program – Low-Income Subsidy. Otherwise, you will pay a monthly premium to the insurance company whose Part D plan you enrolled in.

How much does it cost for Medicare Part D?

The insurance carriers set monthly premiums, and they vary widely. In most states, you can find plans starting around $15/month.

Who is eligible for Medicare Part D?

Any Medicare beneficiary enrolled in either Part A and/or B can enroll in Medicare Part D. You must live in the plan’s service area as well.

Should I Skip Part D?

Our agency does not recommend skipping Part D. Why risk it when most states have plans available for as low as around $15/month? Keep in mind that Part D is insurance not just for your medications today. It also insures you for any new medications that your doctors prescribe in the future.

There are hundreds of medications that cost hundreds or thousands of dollars per year. These would be difficult to afford without coverage. If you are still not sure, please read our article about Why You Need Part D.

At our agency, we provide FREE assistance to our new Medicare clients by analyzing their Medicare Part D drug plan needs and helping them with their initial sign-up for Part D. We then provide ongoing information and instructions on how to use Medicare’s Plan Finder to shop your plan each fall. This exclusive help is limited to our Medigap policyholders ONLY.

Then we’ll provide free claims support for the life of your policy.

Don’t forget that Part D is voluntary! If you wish to enroll, you must contact your agent during a valid election period to initiate the conversation.

Call today for a quick consultation 317-536-8565

Call